Between a Rock and a Hard Place | Keeping Connected

April 20, 2026

The Federal Reserve and investors alike find themselves caught between a rock and a hard place heading into spring. On the one hand, inflation is re-accelerating — headline CPI jumped 3.3% year-over-year in March, driven by a war-fueled energy shock that sent gas prices surging by 21%.

On the other hand, economic growth is losing momentum fast, with Q4 GDP revised down to just 0.5% and global business activity softening from the eurozone to emerging markets. Raising rates risks tipping a fragile economy over the edge; holding steady risks letting inflation become entrenched. March's broad market selloff reflects just how uncomfortable that position has become.

Yet the full picture is more nuanced than the headlines suggest. Beneath the turbulence, the U.S. economy retains genuine pockets of strength. Employers added a better-than-expected 178,000 jobs in March, corporate earnings have now exceeded estimates for twelve consecutive quarters, and U.S. equities — having pulled back to a forward multiple of 20x — offer a more compelling valuation entry point than at any time in recent memory.

Tech is forecast to grow earnings by 45% in 2026, manufacturing activity is expanding, and private credit continues to generate attractive risk-adjusted returns relative to public-market alternatives.

The underlying foundation, while tested, has not buckled. Perhaps most importantly, much of what is weighing on markets today stems from a single source: the conflict in Iran. The war has been responsible for surging energy prices, the spike in global inflation expectations, the selloff in global equities, and the broader cloud of uncertainty that markets have struggled to see through.

History reminds us that geopolitical shocks, however severe, are rarely permanent — and the early April ceasefire has already begun to ease energy prices, offering the Fed a potential window to look through the initial inflation surge and refocus on the underlying trajectory of the economy. A sustained resolution to the Iran conflict would not merely remove a headwind — it could act as a powerful catalyst, unlocking a rapid repricing across risk assets that have been discounting worst-case outcomes.

In the meantime, diversification remains essential, and we believe investors who remain disciplined through the turbulence will be well positioned for what comes next.

U.S. Jobs Market Outperforms in March, but How Big a Risk Is Stagflation?

U.S. employers added a better-than-expected 178,000 new jobs to the economy in March, well ahead of the 59,000 estimate. February's number was revised down by 41,000, while January was revised up by 34,000 to 160,000, putting the 3-month average around 68,000.

The unemployment rate edged lower to 4.3%, though that was largely due to a sharp reduction in the labor force (the labor participation rate fell to 61.9%).

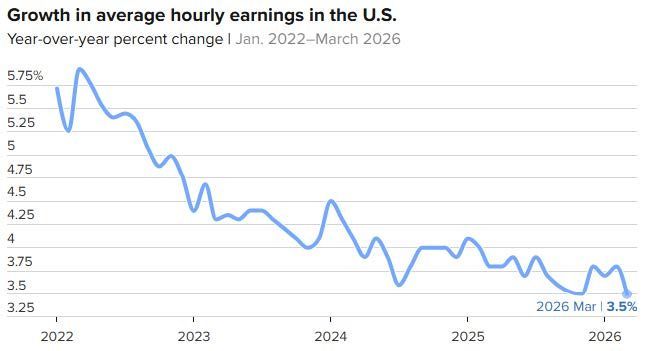

Wages also rose less than expected, with average hourly earnings up just 0.2% for the month and 3.5% from a year ago. Economists had expected respective readings of 0.3% and 3.7%. As has been the case, health care was responsible for much of the growth, adding 76,000 jobs.

Construction saw an increase of 26,000, while transportation and warehousing posted a gain of 21,000. On the downside, the federal government saw a loss of 18,000, while financial activities lost 15,000. The U6 unemployment rate rose to 8%.

The third and final reading on Q4 U.S. economic growth showed further sluggishness. GDP growth was revised down to just 0.5% after surging 4.4% in Q3. Federal government spending and investment fell at a 16.6% annual pace due to the government shutdown, which lopped 1.2% off Q4 GDP growth.

Consumer spending expanded 1.9%, down a notch from the previous estimate and from 3.5% in Q3. Business investment, excluding housing, increased at a 2.4% pace, likely reflecting money being poured into artificial intelligence, but the increase was down from 3.2% in Q3. For all of 2025, the U.S. economy expanded 2.1%.

The anticipated March CPI report showed headline inflation spiked 0.9% M/M or 3.3% Y/Y. Core CPI increased only 0.2% M/M or 2.6% Y/Y. Most of the increase came from the Iran war and the 21% surge in gas prices.

Energy prices have moderated a bit in April with the ceasefire, perhaps allowing the Fed to look through the initial surge in energy costs to focus on the underlying path of inflation, which continues to sit above its 2% target.

Food prices were unchanged for the month and up 2.7% annually, while shelter costs rose 0.3% M/M and 3% annually. The Fed's preferred inflation gauge, PCE, increased 2.8% Y/Y in February, with core PCE rising 3%.

Nature's Symphony

Source(s): U.S Energy Information Administration

Tech Stocks Set to Drive Strong Q1 Earnings

In the very early innings of the Q1 earnings season, the S&P 500 has delivered 12.6% Y/Y growth, slightly behind the 12.8% estimate at the start of the quarter. Earnings have exceeded estimates for 12 straight quarters, and we expect a similar trend to continue, highlighting our thesis that U.S. companies are excellent at managing earnings expectations and guidance.

For 2026, the analyst community expects 17.6% earn-ings growth with 16.4% growth expected in 2027. Tech, materials, and financials are projected to report the highest EPS growth, led by tech, which is forecast to increase earnings by 45%.

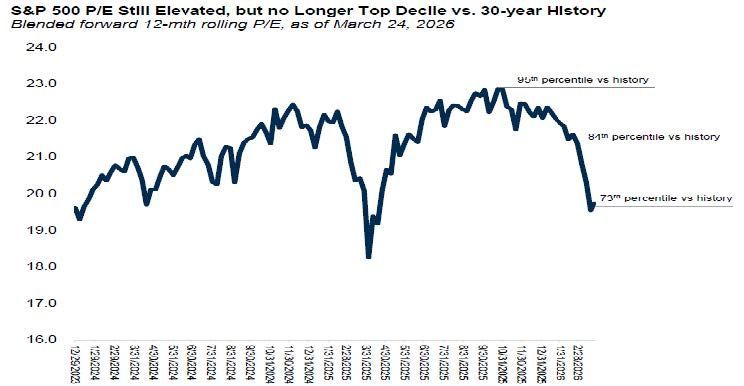

The combination of strong Y/Y earnings growth and the March drawdown has created a more compelling valuation backdrop for U.S. equities, which are now trading at a forward multiple of 20x.

Manufacturing Activity Strengthened, But Services Weakened

The ISM Manufacturing PMI rose to 52.7 in March (up from 52.4 in February). New orders and production gained ground, while employment weakened. The prices component also jumped. Service sector activity weakened slightly in March, with the ISM Services PMI falling from 56.1 in February to 54.0. Production and employment portrayed weakness while prices and new orders strengthened.

Private Credit - Noise or Real Stress

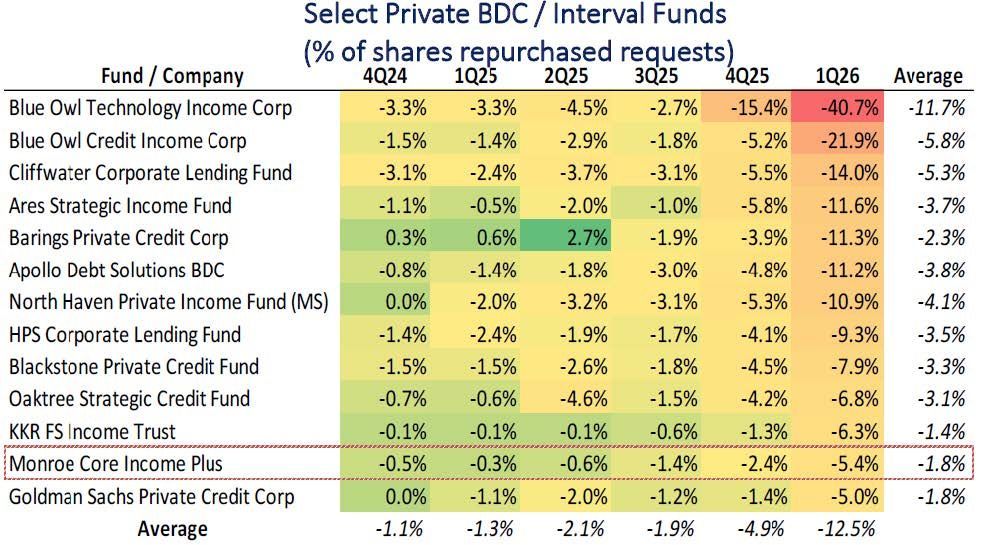

Redemption requests in private credit continue to make headlines as investors seek liquidity from private BDCs, interval funds, and other quarterly liquidity vehicles. Barclays estimates that only 20% of the direct lending market is in these more liquid quarterly-redemption vehicles.

All of the noise around PC right now has occurred within corporate direct lending markets that have seen massive capital flows over the past decade. PC spreads have tightened, particularly in the larger market segments. The Lower Middle Market remains the most attractive due to its ability to command a premium.

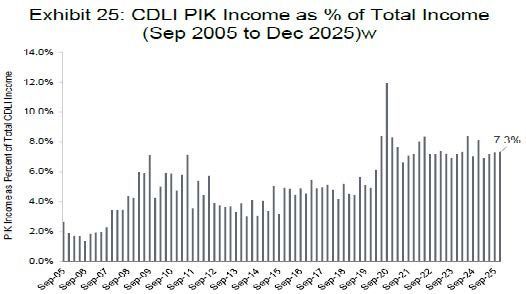

Payment-In-Kind (PIK) income is another indicator of market stress, rising during periods of economic strain and falling during periods of economic growth. PIK peaked during the COVID crisis at 12% in September 2020, but has remained elevated in the 7-8% range since. PIK income is less desirable than cash interest income, and high PIK ratios can signal deterioration in loan quality.

According to JP Morgan data over the past 21 years, the Cliffwater Direct Lending (CDLI) Index has experienced a 1% credit loss rate, compared with 0.93% for leveraged loans and 1.39% for HY bonds. The CDLI Index (9.66%) continues to offer a ~300 bps yield premium over leveraged loans (6.70%) and HY bonds (6.73%).

Nature's Symphony

Source(s): U.S Energy Information Administration

Eurozone Business Activity Softens in March

Business activity in the eurozone softened to a 9-month low in March, perhaps showing the initial impact of the war in Iran. The service sector was the primary source of weakness in March, while the manufacturing sector remained solid.

Within countries, Spain and Ireland registered an acceleration in activity while France and Italy recorded contractions.

After seeing encouraging signs of growth earlier in the year, the March PMI data suggest broader weakness from the Iran war, market volatility, and surging energy prices.

Eurozone growth has likely stalled, and economists expect Q1 GDP growth of just 0.2%.

China's PMIs Remain Weak, Brazil Continues Tough Battle Against Inflation

China's manufacturing sector rebounded in March, posting its fastest pace of activity in more than a year.

The official manufacturing PMI increased from 49.0 in February to 50.4 in March. The report showed that production and new orders expanded while the measures on raw materials inventory, employment, and delivery time remained in contraction territory.

In the first two months of this year, China's exports surged 21.8% Y/Y, sharply beating expectations, as robust demand from SE Asia and Europe more than offset the slump in U.S.-bound shipments. The official non-manufacturing PMI rose to 50.1 in March from 49.5 in the prior month.

Brazil's battle against inflation finally paid off in February, with headline inflation falling to 3.8% (down from 4.4%). The decline was driven primarily by base effects in housing and electricity, where Y/Y increases fell sharply from 10% to 5.7%. However, the monthly reading tells a different story with consumer prices rising 0.70% in February - the largest M/M increase in a year.

The conflict in Iran and Brent crude at about $110 introduce yet another inflationary shock that could plague countries across the globe.

Market Review

- U.S. equities struggled in March, largely due to the war in Iran, higher oil prices, and a surge in inflation expectations. Markets hate uncertainty, and that drove the narrative last month.

- Growth lagged value across all market capitalizations, and there was little dispersion between small caps and large caps.

- After starting 2026 on a positive note, the S&P 500 finished Q1 down 4.3%. There was a strong correlation between higher interest rates and equity market weakness in March.

- Stocks outside the U.S. posted strong gains to start the year but were hit particularly hard in March by the conflict in Iran and a surge in interest rates and inflation expectations.

- EAFE and EM equities lagged their U.S. counterparts last month. Growth trailed value, and small caps underperformed large caps. U.S. dollar strength cost EAFE investors 230 bps of performance in March and EM investors 252 bps.

- Yields on the 10-year Treasury and other global sovereign debt surged higher in March as investors repriced inflation expectations and global risk. The jump in interest rates was negative for core fixed income and municipal bonds. Bonds outside the U.S. were also plagued by USD strength.

- Risk-off sentiment widened spreads across all areas of credit last month. Loans benefited from their floating rate properties, but high-yield and EMD fell in value.

- Hedge funds exhibited broad weakness last month with losses across all major strategy groups. Equity-sensitive funds underperformed macro-driven funds.

- Real assets were a mixed bag in March, with commodities and MLPs posting gains while REITs and GLI fell in value.

- March was a difficult month across most asset classes due to the Iran conflict. Diversification remains crucial, and we believe performance should improve once the geopolitical tensions subside.

Note: For informational purposes only. Not an investment recommendation. The views expressed are those of Meramec Financial Planners LLC's advisory representatives as of the date of this newsletter. Opinions and any forward-looking statements expressed in this newsletter are subject to change without notice and are not guarantees of future performance. Historical performance figures for the indices are provided for illustrative purposes only and do not represent any actual investments. Index performance assumes reinvestment of distributions. The Indices are unmanaged, and you cannot invest directly in an index. Past performance is no guarantee of future results. Diversification does not assure or guarantee better performance and cannot eliminate the risk of investment losses.