How Concerned Should We Be About Labor Markets?

Keeping Connected Newsletter • March 2, 2020

How Concerned Should We Be About Labor Markets?

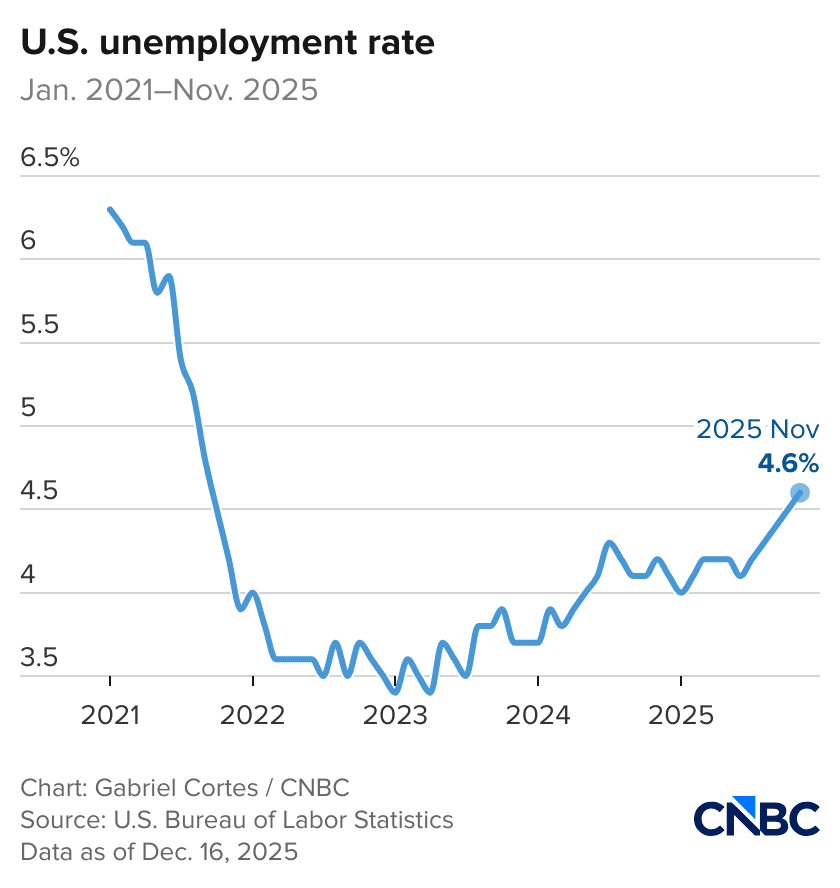

U.S. employers added more jobs than expected in November after the labor market shed 105,000 jobs in October. Job growth totaled 64,000 in November, exceeding the 45,000 estimate, but the unemployment rate rose slightly more than anticipated to 4.6%. A more encompassing measure that includes discouraged workers and those holding part-time jobs for economic reasons swelled to 8.7%, its highest level since August 2021.

The October slump came from a steep fall in government employment as deferred layoffs instituted earlier this year took effect. Government payrolls were off 162,000 for the month and fell an additional 6,000 in November. Average hourly earnings rose just 0.1% M/M or 3.5% Y/Y, the smallest annual gain since May 2021. At first glance, the loss of government jobs and an increase in the labor participation rate are drivers of the higher-than-expected unemployment rate.

Consumers Continue to Lead the Way While Manufacturing Struggles

U.S. retail sales were flat in October versus the prior month, following a revised 0.1% increase in September. Spending clearly moderated after surging over the summer, where sales jumped 0.6% in July and August and 1% in June. Sales at clothing and accessories stores rose 0.9%, while business at furniture and home furnishing stores increased 2.3%, likely due to higher prices driven by tariff costs. Restaurants saw a 0.4% dip in sales. The all-important core retail sales figure, which correlates to consumer spending in the GDP report, jumped 0.8% M/M in October.

The U.S. manufacturing sector further contracted in November, with the ISM Manufacturing PMI falling to 48.2 from 48.7 in October. New orders and employment dragged down the manufacturing sector while production surged back into expansion territory. On the flip side, service sector activity expanded in November, with the ISM Services PMI rising from 52.4 in October to 52.6 in November. New orders slumped, but all other key metrics strengthened. Consistent with global trends, manufacturing remains in a recession, while consumer spending and services remain healthy and supportive of economic growth.

Fed Cuts Again, But Tempers Future Expectations as Q3 Earnings Destroy Estimates

The Fed cut rates again at its December meeting but signaled to investors that there's no guarantee of more rate cuts in the near future. The central bank cut its benchmark federal funds rate by another quarter of a percentage point, bringing it to a range of 3.50% to 3.75%. This cut marks the third reduction this year and means the fed funds rate has now come down by a total of 1.75 percentage points since it peaked in 2023–2024.

This was the fourth FOMC decision in a row that faced at least one formal dissent from a committee member. There were three dissents from this decision, with one member who wanted to cut rates by a greater amount and two who preferred to hold rates steady. The FOMC also raised its median gross domestic product forecasts for 2026 by 0.5%, to 2.3%, while keeping its unemployment projection unchanged at 4.4% and with inflation moving lower by 0.2% to 2.4%. The Fed Fund Futures are pricing in 2-3 rate cuts in 2026, though we believe the Fed will be data-dependent.

One major surprise was the announcement of reserve management purchases starting almost immediately at a pace of $40B per month. The Fed indicated that purchases would remain at this elevated pace for the next few months to build reserves ahead of the April tax date, when the Treasury general account will rise sharply and drain reserves from the banking system. All told, the Fed will be a major buyer of T-bills in the coming months.

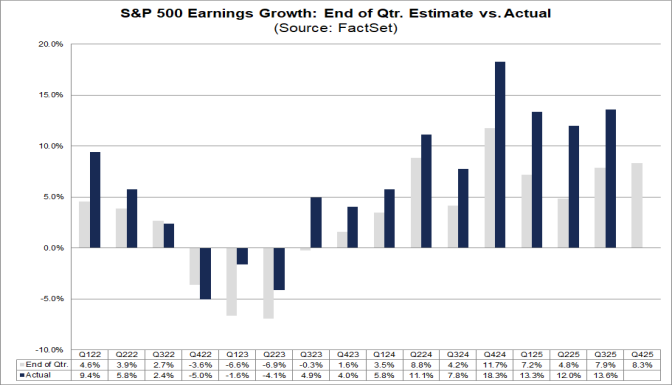

The Q3 earnings season ended well ahead of expectations, with Y/Y growth coming in at 13.6% versus the initial estimate of 7.9%. Earnings are forecast to grow 8.1% in Q4, 12.1% in 2025, and 14.5% in 2026. As always, earnings will be crucial for supporting already elevated U.S. equity valuations. The analyst community expects $309 of earnings for the S&P 500 in 2026, which equates to a 22x forward EPS multiple. We continue to believe our growth-oriented market supports a higher relative multiple compared to EAFE and EM equities. A theme for 2026 is broadening earnings growth beyond the Mag 7.

Services = Strong Manufacturing = Weak, Eurozone GDP Bears Weak Expectations

Eurozone flash PMI data showed that the economic bloc likely ended 2025 on a high note. The HCOB Flash Composite PMI fell from 52.8 in November to 51.9 in December, with services in expansion territory and manufacturing in contraction. New order growth softened amid a sharper reduction in new export business, but companies took on extra staff for the third consecutive month. The eurozone's largest economy – Germany – saw slower output growth in December, while France's output flatlined. The rest of the eurozone again posted solid growth of business activity, although the pace of expansion eased from November. The service sector has helped stabilize the vulnerable eurozone economy, but any uptick in economic growth will need to come from the manufacturing sector.

Eurozone GDP growth for Q3 of 2025 was revised slightly higher to 0.3%, up from the preliminary estimate of 0.2%. The upgrade was driven by a rebound in fixed investment, which rose 0.9% after a 1.7% decline in Q2, and by stronger government spending, up 0.7% after 0.4% in Q2. Inventory changes contributed to Q3 GDP growth while net exports subtracted 0.2%. Spain and France led the expansion in Q3, but German growth remained stagnant.

Remove the Noise & China is an Economic Mess

China's factory activity unexpectedly contracted in November, according to the RatingDog China General Manufacturing PMI, which showed that soft domestic demand continued to cast a pall over the world's second-largest economy. The headline reading of 49.9 in November was down from 50.6 in October. The official China manufacturing PMI showed China's factory activity shrank for an eighth month in November, coming in at 49.2, a slight improvement from 49.0 in the prior month. New orders were weak in November, but new export orders showed a notable pickup. Perhaps of greater importance was the contraction (for the first time since December 2022) in the official non-manufacturing PMI, which comprises construction and services. The headline reading declined to 49.5 in November, signaling weak domestic demand and softness in the real estate sector. The latest economic data suggested China's growth is likely to decelerate further to below 4.5% in Q4 from the 4.8% expansion in Q3.

All Eyes on Oracle's Growing Debt Load

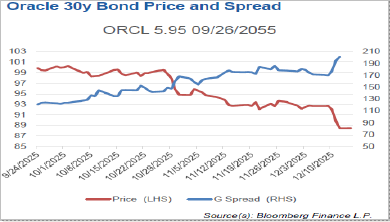

Oracle is perhaps the poster child of the global AI hyperscaler buildout. Many tech companies have been issuing debt to fund the large amount of capex expected over the next few years. Goldman Sachs forecasts $394B of hyperscaler capex in 2025, growing to $619B in 2027. The companies at the forefront of this growth include ORCL, MSFT, ME-TA, AMZN, and GOOGL. Oracle has seen tremendous growth over the past few years, but it has also issued significant debt to finance its AI buildout. Since the company issued its 30-year bond in September, spreads have blown out to near-investment-grade levels. Several experts believe Oracle’s debt will grow from $100B this year to $300B in 2028, and accelerating earnings will be necessary to keep pace with this higher debt load. Remaining investment grade is a key initiative for Oracle.

Market Review

- U.S. equities eked out small gains last month, led by small caps and value stocks. U.S. equities lagged other developed markets in November. Small caps beat large caps, and value stocks outperformed growth stocks across all market capitalizations.

- Stocks outside the U.S. posted modest gains, though some EMs posted outsized losses.

- Within EAFE markets, small caps beat large caps, and value stocks outpaced growth stocks. Value-driven Europe also outperformed Japan. Within EMs, weakness stemmed from China and other Asian EM countries. EM small caps fell 1.4%.

- The weaker USD boosted EAFE returns by 7 bps in November, but USD strength versus EM currencies cost EM investors 79 bps.

- Fixed income markets worldwide benefited from lower interest rates and modest spread tightening in November.

- Core fixed income and muni bonds gained ground, along with all credit sectors, as coupon clipping benefited from higher starting yields.

- Bonds outside the U.S. saw an added boost from a slightly weaker U.S. dollar during November.

- Hedge funds broadly gained 0.7% in November, led by equity long/short and global macro strategies. Event-driven funds lost ground, and relative value funds eked out small gains. Hedge funds have produced solid returns in 2025 across most key strategies while providing downside protection and diversification.

- Real assets had a pretty strong month overall with gains in listed infrastructure, REITs, MLPs, and commodities.

- Diversification remains the theme for 2025, as almost all asset classes have contributed to solid performance throughout the year. As we look towards 2026, the economic and market backdrop remains supportive for equities and other risk assets.

Note: For informational purposes only. Not an investment recommendation. The views expressed are those of Meramec Financial Planners LLC's advisory representatives as of the date of this newsletter. Opinions and any forward-looking statements expressed in this newsletter are subject to change without notice and are not guarantees of future performance. Historical performance figures for the indices are provided for illustrative purposes only and do not represent any actual investments. Index performance assumes reinvestment of distributions. The Indices are unmanaged, and you cannot invest directly in an index. Past performance is no guarantee of future results. Diversification does not assure or guarantee better performance and cannot eliminate the risk of investment losses.